Key Takeaways

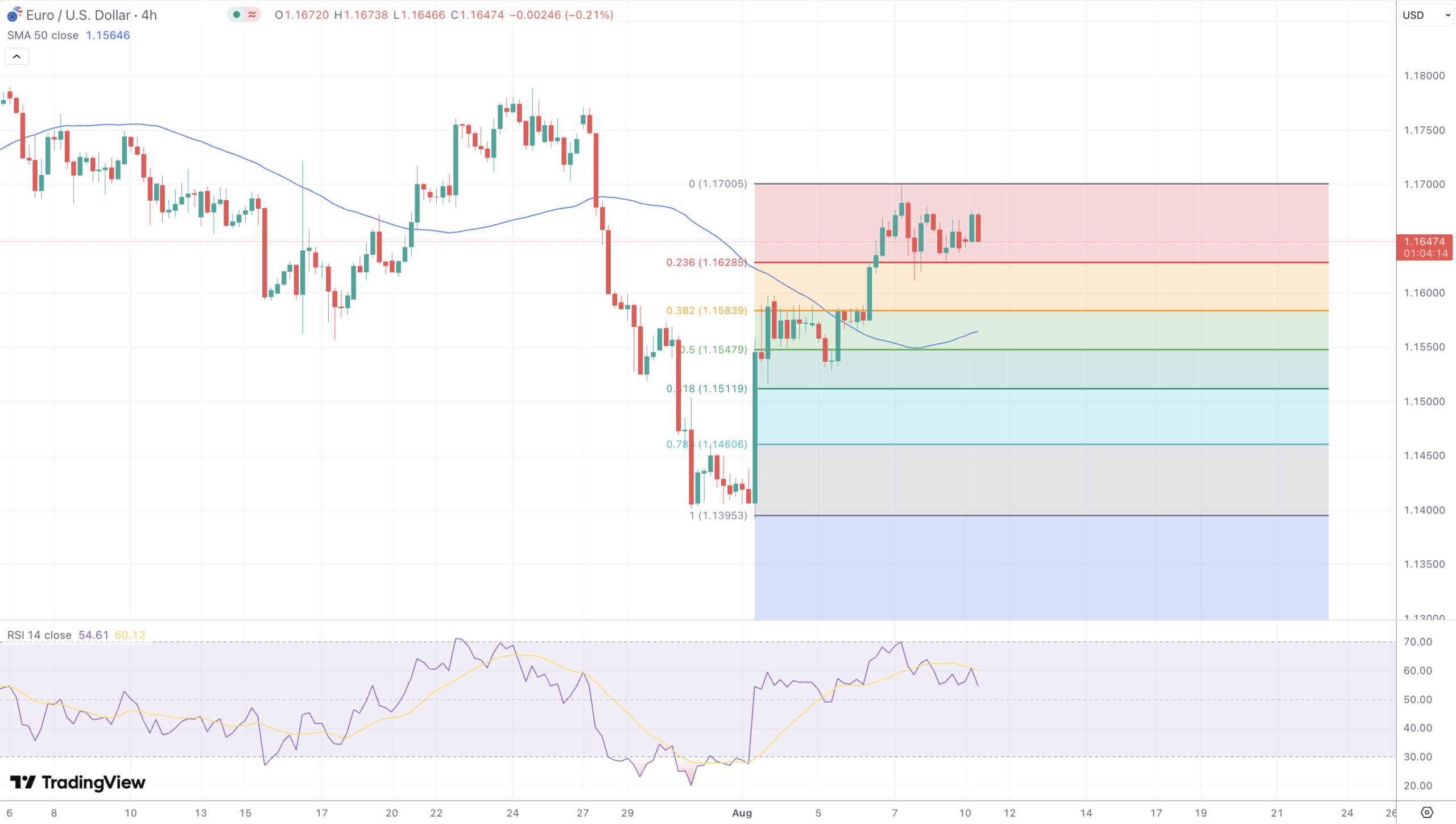

- EURUSD starts the week near 1.1640 to 1.1670, with dip buying showing up ahead of U.S. CPI.

- Resistance sits at 1.1700, then 1.1760 to 1.1800, while support layers at 1.1620 to 1.1600, then 1.1565, 1.1533 and 1.1500 from Fibonacci of the 1.1395 to 1.1670 leg.

- Key data this week includes U.S. CPI on Tuesday and PPI Thursday, plus Germany and euro area ZEW on Tuesday and euro area industrial production on Thursday.

- Euro area inflation holding at 2 percent keeps the ECB comfortable staying on hold, so the dollar side and U.S. data remain the main swing factors.

Market Dynamics and Recent Performance

EURUSD starts the week trading around 1.1640 to 1.1670 after a steady climb from the early-August trough near 1.1395. The move higher has been helped by a softer dollar into Tuesday’s U.S. CPI release and lingering expectations for a September Fed cut. Headline euro area inflation held at the ECB’s target in July, reinforcing the idea that Frankfurt can stay patient after its recent easing cycle, while the dollar side of the pair is swinging with tariff headlines and questions around Fed credibility. Into the data, the dollar index is hovering just above 98 and risk assets are stable, keeping the euro bid on dips.

Technical and Fundamental Influences

From a price-action lens, the pair is riding a short-term uptrend, with higher lows from 1.1395 and a series of failed attempts to break below 1.16. Immediate resistance sits at 1.1700, then 1.1760 to 1.1800, which lines up with the top of the 52-week range. Nearby support is layered at 1.1620 to 1.1600, then 1.1565, 1.1533 and 1.1500. Those latter three levels are the 38.2 percent, 50 percent and 61.8 percent retracements of the rebound from 1.1395 to 1.1670, which creates a clean confluence if U.S. data jolts the dollar higher. A sustained close above 1.1700 would expose the 1.1760 to 1.1800 pocket, while a break under 1.1565 would warn of a deeper pullback toward 1.1500.

Macro cues dominate this week. The U.S. CPI for July lands on Tuesday, followed by PPI on Thursday. In Europe, the ZEW surveys hit on Tuesday and euro area industrial production arrives Thursday. Softer U.S. core inflation would typically push real yields down and the dollar lower, favoring a push toward 1.1760 to 1.1800. A hot core print would likely cap rallies near 1.1700 and put the 1.1565 to 1.1533 zone in play. Sentiment is also sensitive to the U.S. tariff deadline and broader geopolitics, which have been adding headline noise to dollar swings.

On the euro side, July inflation sticking at 2 percent supports the ECB’s hold-steady stance for now, keeping policy-rate differentials from widening back in the dollar’s favor unless U.S. inflation surprises. Short-dated options activity is clustered around 1.1650 to 1.1600 and 1.1500 this week, which can act as magnets into the 10 a.m. New York cut and occasionally firm those supports or caps intraday.

Looking Forward

Base case for the next few sessions is a two-way market centered around 1.1650 with CPI setting the break. If CPI cools, expect a grind through 1.1700 and an attempt at 1.1760 to 1.1800. If CPI runs hot, look for sellers to defend 1.1700 and push price back into 1.1600 to 1.1530, where the Fibonacci cluster and prior demand overlap. ZEW surprises and euro area industrial production could skew the second-leg move after Tuesday, but the first impulse likely belongs to U.S. inflation.